The novel IFICI+ fiscal boon in Portugal was instituted with the objective of enticing exceptionally proficient experts from foreign lands to the nation, alongside augmenting the indigenous commercial collective. Corporate enrollment in Portugal is a prevalent custom amidst entrepreneurial organizations endeavoring to capitalize on Portugal business jurisprudence and to cultivate a labor force of exceptionally adept and dynamic individuals.

This phase permits enterprises not solely to acquire ingress to a propitious juridical structure overseeing mercantile undertakings in Portugal, but also to exploit the prospect to allure adept professionals with the requisite expertise in avant-garde sectors and the drive to attain triumph. Specifically, Portugal corporate legislation is adaptable and pellucid, engendering permissive circumstances and enabling Portugal to be incorporated into the “Preeminent nations to reside” for industrialists and laborers.

The IFICI+ fiscal arrangement inaugurated in Portugal, denominated “Incentivo Fiscal para a Inovação e Criatividade Internacional.” This schema is formulated to engender preferential conditions for individuals contemplating the establishment of an enterprise in Portugal or deliberating this jurisdiction to execute their vocational undertakings. Recipients of the IFICI+ paradigm in Portugal are endowed with the entitlement to avail themselves of specific fiscal privileges, thereby augmenting the yield on capital infusion and propelling the advancement of ingenuity.

IFICI - the novel pecuniary framework in Portugal codified in Government Regulation No. 352/2024/1 from December 23. Its instantiation aided in Portugal attaining one of the foremost stations against the tableau of European realms alluring for expatriation.

Particulars pertaining to the stipulations of the IFICI regime in Portugal may be discerned through perusal of the treatise.

Portugal is a thriving center for research and innovation

The Portugal economy is undergoing an energetic phase of expansion, typified by an elevated degree of ingenuity endeavors, with the metropolis of Lisboa spearheading the charge, asserting its standing as a preeminent European hub of ingenuity. Throughout the preceding decennium, there has been a prodigious surge in capital infusion into nascent undertakings within the nation, manifested in a mean annual escalation of 30%. This datum elucidates a momentous augmentation in growth velocities observed in alternate European metropolises, which intimates the existence of a propitious capital influx framework and the allure of this dominion for speculative financiers.

Key sectors experiencing rapid growth:

- Technological and Information and Communication Technology (ICT). Lisbon and Porto are principal technological epicenters, drawing expertise from throughout Europe and further afield.

- Health sciences and biotechnological advancements. The nation’s biotechnological domain is expanding swiftly, with scholarly establishments and nascent enterprises concentrating on pioneering healthcare remedies.

- Ecological technologies and sustainable power reserves. Portugal stands as a vanguard in sustainable energy, rendering it a compelling locale for practitioners in the ecological technology sphere.

Fiscal ordinances in Portugal are typified by an elevated extent of pecuniary emancipation and the allocation of substantial tax prerogatives, owing to which, the domain is becoming enticing among expatriates from European sovereignties.

Tax regime for new residents in Portugal IFICI+

The novel IFICI levy system has materialized in Portugal, intended to inaugurate vocational associations with acknowledged field authorities inclined towards translocation for inquiry and innovation. To engage as a contender in the system, one must satisfy a multitude of stipulations, encompassing possession of an academic credential and expertise in the pertinent domain. Moreover, ante-registration with the revenue bureau of the Portuguese Commonwealth, alongside the submission of corroborative papers, is indispensable, coupled with validation by the patron.

There exist assemblages of scholarly cognoscenti in the Commonwealth, which are chiefly congregated in substantial metropolitan hubs. In the purview of effectuating entrepreneurial emigration to Portugal or relocating to engage in erudite vocations, or for entities classified as cybernetic itinerants, Madeira emerges as the premier selection amongst autonomous practitioners from foreign dominions to fulfill their aspirations. The NHR 2.0 ordinance in Portugal in the annum 2025 permits the deployment of mutable fiscal imposts, which aims to forge optimal circumstances for the conveyance and execution of avant-garde methodologies.

System with distinct IFICI fiscal abatements in Portugal institutes a 20% levy on vocational earnings. undertakings for a decade. This notion encompasses emoluments procured from autonomous vocational engagements, such as scholarly, technological, and other vocations necessitating esoteric expertise and acumen. Nevertheless, should the emoluments originate from sources beyond Portugal, excluding annuities, then no fiscal imposition is enacted at the national stratum, provided the emoluments are disclosed in the revenue declaration. Yet, individuals who have antecedently utilized concessions under NHR and analogous frameworks are precluded from eligibility for the IFICI arrangement.

Crucial! The fiscal advantage is granted solely a singular instance.

Comparison IFICI+ mode in Portugal and the former NHR

The NHR regime, instituted within the Portuguese juridical structure in 2009, constitutes a preferential fiscal apparatus designed to confer pecuniary advantages to extrinsic persons and denationalized entities satisfying prescribed conditions for a span of 10 annums. This system accorded the ensuing privileges for novel inhabitants:

- Expatriation of dormant revenue from the fiscal framework. For a decade, nascent inhabitants luxuriated in total fiscal exemption on the majority of strata of dormant revenue originating from extrinsic domains. This clause broadened, yet was not confined to, rental remuneration, pecuniary returns, and dividend earnings, alongside capital increments.

- Fixed pecuniary revenue levy rate. Rather than a gradated impost for pecuniary revenue levies, the apex quantum of which might attain 48%, a 20% surcharge was imposed on the earnings of nascent inhabitants.

- Tax abatements on annuities. Annuity reserves procured from alien sources were liable to levies at a 10% surcharge.

The Portugal fiscal system NHR 2.0 (IFICI) in 2025 exhibits distinct variances from the antecedently employed NHR, specifically, it is concentrated on the ingress of expatriate virtuosos from their technological domain, erudition investigators, and academic instructors. The prior NHR structure was more ubiquitous and attainable to a broad array of individuals inclined to relocate to Portugal.

To attain NHR 2.0 stature, requisites are delineated for each particular domain of enterprise. The IFICI+ fiscal framework in Portugal governs limitations on categories of revenue eligible for privileges. Broadly, the distinctive tax paradigm of Portugal IFICI+ — an exquisitely focused mechanism for luring overseas experts, which diverges from the antecedent iteration through obligatory stipulations for credentials and constraints on revenue types.

|

NHR |

IFIC |

|

|

Tax on business activities with a significant level of added value |

20% |

|

|

Taxation of the income of individuals belonging to the professorial or teaching pool, scientific researchers, start-ups, persons holding positions recognized by the EPE and IAPMEI is carried out at a differentiated rate, providing for an increase in the tax burden in proportion to the increase in income, with a maximum rate of 53% for income not related to the main activity. |

||

|

Taxation of pension accruals |

10% |

Portuguese tax regime IFICI+, unlike its predecessor NHR regime, excludes pension income from its scope and concentrates exclusively on the earnings of qualified overseas workers, which represents a significant change in approaches to taxation of this category of persons. |

|

Dividend tax |

0% |

|

|

Capital gains tax on movable property |

28% |

0% |

|

Capital gains tax on real estate |

0% |

|

|

Tax on income arising from rental property |

||

|

Tax on profits received from assets located in preferential tax zones |

35% |

|

The antecedently pertinent Non-Habitual Resident schema has protractedly functioned as a potent instrument for luring aptitude by bestowing inducements for dormant income, thus engendering preferential circumstances for fiscal influx and the arrival of technical virtuosos, attenuating pecuniary encumbrances. Incidentally, tax domicile in Portugal is ascertained, firstly, by remaining upon the national domain for a span surpassing 183 days, computed both successively and cumulatively, within 12 revolutions of the sun, the commencement or culmination of which coincides with the relevant solar calendar annum; secondly, the existence within Portugal of a habitation which, by its peculiarities and contingencies, denotes the individual’s proclivity to designate it as a locale of uninterrupted habitation.

In particular, the NHR regime provided the following benefits:

- No disbursement, gain, lease remuneration or capital appreciation levies.

- Diminished impost (20%) for revenue from labour and entrepreneurial endeavors accrued within the Republic.

- Opportunity to invoke Double Taxation Agreements forged by Portugal with alternate sovereignties.

- To procure NHR designation, it was requisite, inter alia, to not have been a fiscal domicile of this polity for the antecedent quinquennial and to possess a lawful entitlement to domicile in the nation.

The NHR regimen assumed a paramount function in the economic affluence of the polity. However, in 2023, the administration proclaimed a gradual forsaking of it, and in 2024, the adept authorities executed fiscal metamorphosis, climaxing in the instatement of the novel IFICI+ pecuniary privilege in Portugal, concentrated on further advancement and amelioration of fiscal canons.

IFICI+ program requirements in Portugal

The IFICI+ modus in Portugal instituted privileges for individuals who satisfy fiscal residency stipulations. This system has previously drawn savants of the uppermost echelon who have selected this nation for permanence and protracted labor. Portuguese fiscal domicile under the IFICI system is accessible to a body if it fulfills a multitude of conditions. Initially, it is requisite to substantiate the nonexistence of fiscal resident status of this polity throughout the preceding quinquennial fiscal intervals. This stipulation is compulsory and is beyond annulment.

Secondly, the petitioner must undertake endeavors that entail procuring remuneration from employment or an autonomous vocation. Endeavors conducted sans subjugation to a labor pact. Concurrently, the enterprise must be acknowledged by the authorized governmental entities as of eminent proficiency. To substantiate tax domicile status, an individual must submit pertinent attestations verifying the fulfillment of the aforementioned stipulations. Should a solitary criterion be unfulfilled, Portuguese fiscal domicile cannot be ascribed.

Representatives of professions in priority areas:

- Instructors at academies, scholarly investigators (abstract and pragmatic endeavors). This classification encompasses the entitlement to gainful occupation in institutions and involvement in the governance of technologic or avant-garde commercial organizations.

- Occupations that satisfy codified proficiency stipulations (enumerated beneath), in the context of formal pacts that confer distinctive immunities.

- Individuals in occupational affiliations whose vocational responsibilities have been validated by authoritative entities such as AICEP and IAPMEI as pivotal to the advancement of protracted fiscal equilibrium on a national scale, encompassing individuals executing vocational proficiencies in autonomous territories, adhering to the stipulations prescribed by the regional regulatory framework.

- Technological virtuosos whose Research & Development expenditures may be utilized to ascertain fiscal incentives to foster the evolution of knowledge-centric domains.

In IFICI+ configuration in Portugal Encompasses experts from foreign nations contracted by Portuguese certified nascent enterprises that satisfy the subsequent prerequisites:

- the tally of personnel doth not surpass 250 operatives;

- yearly income doth not surpass 50 million EUR;

- the span of commerce doth not transcend 10 years if the principal bureau is situated within Portugal or the nascent enterprise possesseth a certified native proxy establishment.

Substitute structure: nascent enterprises in Portugal ought to possess an excess of 25 indigenous laborers. These nascent enterprises must not be constituted via corporate reconstitution. For adept vocations (exemplified hereafter), these encompass:

- Pursuits linked to the extraction of geological commodities and fabrication of substances.

- Voyage and concomitant undertakings.

- Informatics and allied vocational services.

- Agriculture and sylviculture, cultivation, akin domains.

- Investigation and Development, alongside endeavors pertaining to the deployment of advanced technologies.

- Manufacture of acoustic and multimedia compositions.

- Sectors of defense, ecological safeguarding, power domain.

In the purview of the inception of the IFICI+ schema in Portugal, vis-à-vis nascent enterprises, concomitant with instituted numerical curbs, there subsists an imperative to substantiate inventive potentiality and the competence to ensnare extraneous capital infusion. Specifically, attestation of the manifestation of an avant-garde commercial paradigm is requisite, in alignment with the stipulations enshrined in Edict No. 195/2018 dated July 5th. Alternatively, corroboration of the National Innovation Agency (ANI) endorsement of appropriateness to embark upon Research & Development may be furnished.

The novel IFICI+ fiscal schema in Portugal pertains to emergent enterprises that have triumphantly finished at least one tranche of venture capital backing from a juridical body authorized to perform venture capital allocations and governed by the regulatory oversight of the CMVM or an adept international authority. In lieu of this, the enterprise may present verification of capital infusion from the Portuguese Development Bank (BPF) or assets curated by the latter. The aforementioned stipulations are designed to furnish sustenance to auspicious startups.

"Motivation for Scholarly Inquiry and Ingenuity" in Portugal institutes qualification prerequisites for petitioners, the principal of which is a scholarly credential or an undergraduate certification, contingent upon scholarly undertakings in the designated domain for a duration of 3 years. The IFICI Endowment subsidizes experts engaged in international trade enterprises. Such fiscal bodies are distinguished by possessing a proportion of foreign trade revenues equating to no less than 50% of aggregate gross receipts, extraordinarily specialized operations in the sectors of manufacturing, informatics, and research and development.

Note. The Portuguese Taxonomy of Occupations (PTO) is a classificatory schema employed to categorize vocations and is pivotal for the application of this fiscal advantage. CAE, that is, Código de Atividade Económica, is a cipher utilized to classify and designate mercantile undertakings in Portugal.

The Portuguese IFICI+ mode is an altered apparatus of inducements, yet the inclusion stipulations have experienced considerable metamorphoses, rendering it unfeasible for recipients of the NHR schema, who presently benefit from fiscal concessions, to meet the qualifications for reductions governed by the novel system.

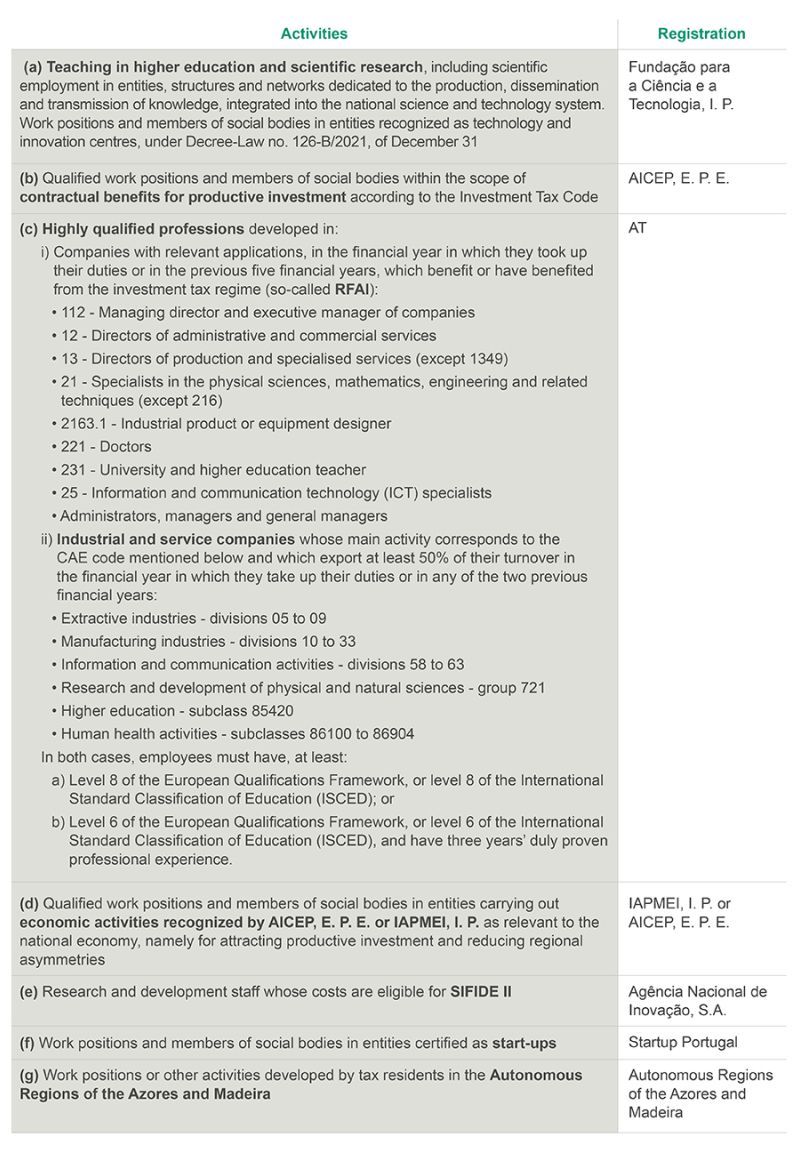

Agencies authorized to verify the compliance of candidates with the criteria for receiving the IFICI+ tax benefit in Portugal:

- The Fiscal Bureau (Autoridade Tributária e Aduaneira), which oversees adherence to the juridical stipulations for petitioners engaged in enterprises involved in extrinsic economic endeavors, wherein the magnitude of export dealings comprises 50% of the aggregate turnover.

- Sectoral oversight entities that execute the process for verifying the entitlement to professional undertakings within the pertinent domain.

- Startup Portugal, which is vested with the authority to authenticate the qualifications of executive members and personnel of validated nascent enterprises.

- AICEP or IAPMEI, providing affirmation of the entitlement to assimilation into a scheme directed at individuals occupying managerial and administrative positions within institutions whose operations are acknowledged as nationally pivotal.

In the event of any alteration in the condition of a taxpayer utilizing the IFICI+ fiscal system in Portugal, the taxpayer is mandated, within an allocated interval, to dispatch a written communique regarding such alteration to the pertinent authority that governs and oversees the undertakings encompassed within the delineated system. The missive must encompass exhaustive and verifiable details concerning the essence and contingencies of the modification in the professional condition of the taxpayer, along with substantiating documentation of such alterations. Neglect or tardy execution of this responsibility may provoke the imposition of sanctions stipulated by prevailing statutes. For individuals contemplating emigration to Portugal, the IFICI system serves as a stratagem to mitigate tax liabilities.

In conformity with ordinances of the IFICI framework within the Portugal Dominion, ingress therein is contingent upon the obligation to adhere to the prescribed methodology for governmental enrollment as a fiscal entity. To consummate the aforementioned process, one must present to the fiscal bureau or the AICEP/IAPMEI Institution a pertinent solicitation, composed in accordance with the stipulations of extant statutory provisions.

All individuals procuring fiscal domicile of a specified realm for the inaugural instance are mandated to tender a petition for allotment of their condition in congruence with the prescribed method of IFICI Portugal. This petition must be tendered to the adept fiscal organs no later than the 31st of March in the annum succeeding the annum in which these individuals procured fiscal domicile status. Once the petition is scrutinized and ratified by the adept organs, IFICI condition comes into effect during the fiscal annum in which the petitioner procured it and is operative for the ensuing decennium.

To ascertain the postulant's adherence to the stipulations promulgated by the canons of prevailing statutory provisions, an all-encompassing compendium of attestations stipulated in the juridical edicts directing the protocol for institutionalization and functioning of the IFICI organizational and technical apparatus must be appended to the petition for governmental enrollment. Inauguration of the IFICI dominion in Portugal methodically fortifies the standing of this polity as a locus sought-after on the European expanse for exceptionally erudite professionals and commercial magnates.

Singular characteristic of the Portuguese fiscal dispensation IFICI+ — entrusted to the legislators of Madeira and the Azores the privilege to devising supplementary legal principles for individuals functioning within their domains. This regulatory sovereignty offers the outlook of malleable enforcement of fiscal preferentials and amplifying prerogatives under the extant dispensation. It is advocated that you consult accredited juridical advisor to procure contemporary intelligence and evaluate the potential prospects and hazards connected with the enactment of the IFICI+ fiscal dispensation in assorted provinces of Portugal.

Contact our experts and get answers to your questions.

Document requirements for registering as a Portuguese tax resident

Prognostications concerning the IFICI paradigm in Portugal epitomize prevailing tendencies in bolstering erudite advancement and technologic ingenuity. To enroll under the stipulations of the IFICI+ fiscal ordinance in Portugal, it is requisite to present to the regulatory body:

- A authenticated facsimile of the labor pact (if existent).

- A legitimate mercantile attestation denoting lawful involvement in the societal supervisory schema.

- An authenticated facsimile of the accord concerning the procurement of fellowship endowments for subsidizing Research and Development.

- Verification of requisite scholastic qualification.

- An assertion formulated by employers and contracting parties under remunerated agreements with IFICI recipients, incorporating delineated actions that align with the stipulations of subsections (b)-(e), exemplified supra within the composition.

- Supplementary manuscripts solicited by empowered entities.

In accordance with the stipulations of the prevailing juridical enactments of the Portugal Commonwealth, entities engrossed in the utilization of alien labor in roles necessitating elevated competencies must undergo scrutiny via a bespoke digital apparatus, administrated by the Portugal fiscal authorities. For manufacturing and service-oriented establishments, this scrutiny protocol encompasses, inter alia, ascertaining the degree to which the quantum of export exchanges adheres to the demarcated limits prescribed by statute, and scrutinizing the consonance of the corporations' undertakings with the stipulations imposed on the domains of activity encompassed by specific normative frameworks.

What characteristics determine Portugal's place in the perception of business and professionals?

Translocation to Portugal is typified by amplified requisition among eminently skilled practitioners and constituents of commercial echelons in foreign nations. This propensity is ascertained by an amalgamation of determinants, encompassing pecuniary inducements, a steadfast juridical milieu, an elevated calibre of existence, and groundbreaking advancements in the economic sphere.

Economic attractiveness:

- Optimal tariff stratagem in the domain of habitation in juxtaposition with Occidental European nations.

- Monetary inducements for external, highly niche professionals and commercial agents, in part, Portuguese IFICI+ schema, permitting the diminution of fiscal encumbrances on revenue accrued beyond the borders.

Social infrastructure:

- Exquisite medical assistance aligns with European Union criteria.

- The existence of proficiently furnished aerial transit infrastructure in Lisbon, Porto, Faro, a cultivated web of thoroughfares and railways, guarantees the convenience of peregrination within the nation and beyond.

Opportunities for erudition are marked by the existence of global academies proffering pedagogical curricula contrived in congruence with cosmopolitan protocols and proffering tutelage in sundry idiomatic frameworks. Portugal was positioned 7th in the preceding annum's Universal Tranquility Register, evincing notable triumphs in the domain of jurisprudence and fortifying the fortitude of civic establishments. This datum can be construed as corroboration of an elevated quotient of efficacy in the civil governance mechanism, as well as a consequence of the coherent execution of juridical mandates and doctrines designed to uphold communal security.

Extramural individuals' fascination with acquiring a domicile authorization in Portugal owing to a diminished consumer price ratio, which, subsequently, dictates the enthusiasm of persons endeavoring to optimize the excellence of existence by alleviating pecuniary outlays. As per the data encompassed in the preceding annum’s release of the Cost of Living Index, the Portugal Commonwealth is positioned amidst European nations distinguished by a superlative equilibrium between the expenditure and caliber of life, which manifests in reduced valuations for real property, nourishment commodities, and other consumer provisions, in contrast to the regional norm. In the prior annum’s investigation, the Portugal Commonwealth secured the 6th position for life caliber (depicted below).

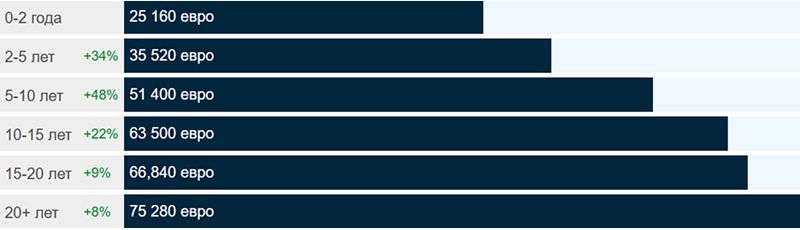

The novel fiscal structure for expatriates in Portugal IFICI draws a considerable cohort of European professionals. The outcomes of an inquiry into the Portuguese workforce, executed via querying employers and employees engaged in R&D, demonstrate that the median yearly earnings of professionals in this domain are EUR 50,200. A scrutiny of the gathered intelligence unveiled a statistically consequential correlation between compensation and tenure.

The illustration above shows that the salary of an R&D engineer will increase by 9% (according to experts) over 5 years.

Thus, specialists who are at the beginning of their professional career (from 2 to 5 years) receive approximately 35 thousand EUR per year. At the same time, highly qualified research engineers with impressive work experience (over 10 years) can count on significant compensation, reaching EUR 63,500 per year (illustrated below). This study allows us to state that there is a pronounced differentiation in the remuneration of R&D specialists in Portugal, depending on their professional experience.

It should be noted that the technology sector is growing this year, reaching 8% of GDP, with the areas of cloud computing and cybersecurity occupying leading positions in the ranking of the highest paid professions. Remuneration for cybersecurity experts and cloud specialists ranges from 55,000 to more than 100,000 euros per year. Lisbon and Porto are becoming hubs of innovation, attracting international corporations and producing 90,000 technical graduates each year. The dynamic system offers lucrative opportunities with significant growth potential in Portugal's expanding digital landscape.

Others changes to Portuguese tax legislation in 2025

Registration of a company in Portugal gives business entities the opportunity to carry out their activities in a stable and impartial legal system, where the principles of the rule of law and the protection of investments guaranteed by the country’s membership in the EU apply. Obtaining a residence in Portugal opens access to the European space, which creates preferential conditions for diversifying a portfolio of assets and establishing cross-border connections.

In order to stimulate the influx of direct investment and strengthen the capital structure of legal entities, a new fiscal mechanism has been introduced into the tax legislation: shareholders are given the right to apply a tax deduction in the amount of 20% of the amount of funds invested by them in the authorized capital of the companies they own. Digitalization of administrative procedures, including the transfer of public services to a digital format, is a priority area of government policy, helping to reduce the bureaucratic burden on business.

In the realities of globalization and digitalization, Portugal occupies a leading position among countries for digital nomads and senior management seeking relocation. Portugal has modern infrastructure to meet the needs of remote workers. Specialized centers for remote workers have been created in Ponta Delgada (Azores) and Madeira, equipped with high-speed data infrastructure and comfortable workspaces. These centers are designed to provide a supportive environment for professionals working remotely, with a focus on ensuring seamless communication and productivity.

Lisbon, Cascais, Porto, Braga, Silver Coast, Algarve, and Comporta persist as captivating locales for digital wayfarers. These territories are distinguished by the existence of a propitious sociocultural milieu and an elevated standard of existence. This vogue is attributable to an assemblage of actions undertaken by the administration, notably, the initiative Digital Nomad Visa Portugal, which grants an exclusive visa regimen for digital wanderers, and a schema of fiscal inducements intended to galvanize the undertakings of fledgling experts.

With the mounting inundation of digital wanderers, youthful clans, and enterprisers into metropolises like Lisbon, Braga, and Porto, the opulent realty sector is undergoing a notable surge. This proclivity is propelling the erection of superior domiciles, frameworks, and lease provisions, whilst the administration's nascent juvenile-centric habitation scheme is crafted to guarantee its allure for arriving adept laborers.

Implementation investment in real estate in Portugal, especially within the island of Madeira, appears to be a strategically sound decision. The competitive cost of assets, coupled with a steady increase in investment demand, creates the prerequisites for increasing socio-economic well-being and obtaining material benefits.

Attracts special attention Portugal's new tax program IFICI+, provided for in the 2025 budget. Modernizing policies to reduce the fiscal burden on corporate structures and introduction of the preferential IFICI+ regime in the Portuguese Republic, are designed to stimulate the development of innovative areas, strengthening the global reputation of this country as a place for talented professionals. IFICI regime in Portugal gives individual entities the right to take advantage of many tax preferences.

Possible competition for foreign talent

The resolution of Portugal regarding the instatement of IFICI fiscal inducements for erratic denizens might exert a substantial influence on the EU's migratory doctrines. This antecedent could function as a spur for EU constituent nations to reconsider their individual tactics for luring adept overseas professionals. Portugal's maneuver underscores an evident inclination towards augmented rivalry amongst EU territories to procure expertise from the global stage. Consequently, the transference of proficient labor might evolve into a more cutthroat process, potentially culminating in more stringent prerequisites and discernment standards.

It should be acknowledged that in the framework of worldwide rivalry for exceptionally skilled manpower, EU constituent nations might be coerced to instigate analogous pecuniary inducements or alternative advantages to preserve their investment allure for overseas experts. Notwithstanding, this procedure elicits the conundrum of securing harmony of levying policy within the EU. The NHR arrangement antecedently enforced in Portugal has been disparaged by several Member States, which have commenced a discourse on equitable fiscal rivalry. In spite of the alteration of this arrangement, latent discordances pertaining to its repercussions on the taxation structures of other EU member states endure.

Conclusion

Portugal provides potentially beneficial opportunities for optimizing tax obligations, but the real implementation of the benefits is achieved only through the development and implementation of a comprehensive, personalized strategy that takes into account the specific circumstances of each individual taxpayer. For expats seeking to optimally adapt to Portugal, a comprehensive understanding of the nuances of its tax system is important. The peculiarity of Portuguese taxation lies in its progressive nature and the introduction of a number of tax preferences. Detailed planning and professional advice are essential to maximizing fiscal benefits.

In 2025, the new IFICI+ tax regime came into force in Portugal., designed to help improve the investment reputation of the state. The proposed package of tax discounts is being implemented to increase the influx of highly qualified specialists with significant intellectual potential into the country. But this program regulates certain restrictions. For example, persons whose income comes from jurisdictions included in the list of offshore zones are subject to a higher tax rate (35%). In addition, IFICI+ regime in the Republic of Portugal is not applicable to taxpayers who have previously availed NHR benefits.

Qualified specialists of our company have the competence to conduct a detailed analysis of all aspects and provide comprehensive legal consultations on the specifics of the special IFICI+ tax regime in Portugal, including its legal regulation, fiscal preferences and procedural nuances.